Vail Resorts Financials Unpacked: Fiscal Year 2024

For the past few years, the largest ski resort operator in the world has been none other than Vail Resorts. This massive ski conglomerate owns and operates more than two dozen ski areas across North America, Australia, and with recent acquisitions in Europe, the company may not look like it’s going anywhere at a first glance. But recently, a few circumstances have raised some questions about whether some chinks are forming in Vail Resorts’ armor.

So what’s really going on, and is Vail Resorts operating as a truly sustainable business? Well, in this piece, we’ll figure this out by going through Vail’s 2024 Earnings Report, and we’ll walk you through how its trends will affect skiing and riding for those visiting one of the 40+ resorts around the world operated by Vail Resorts.

FY ‘24 Revenue

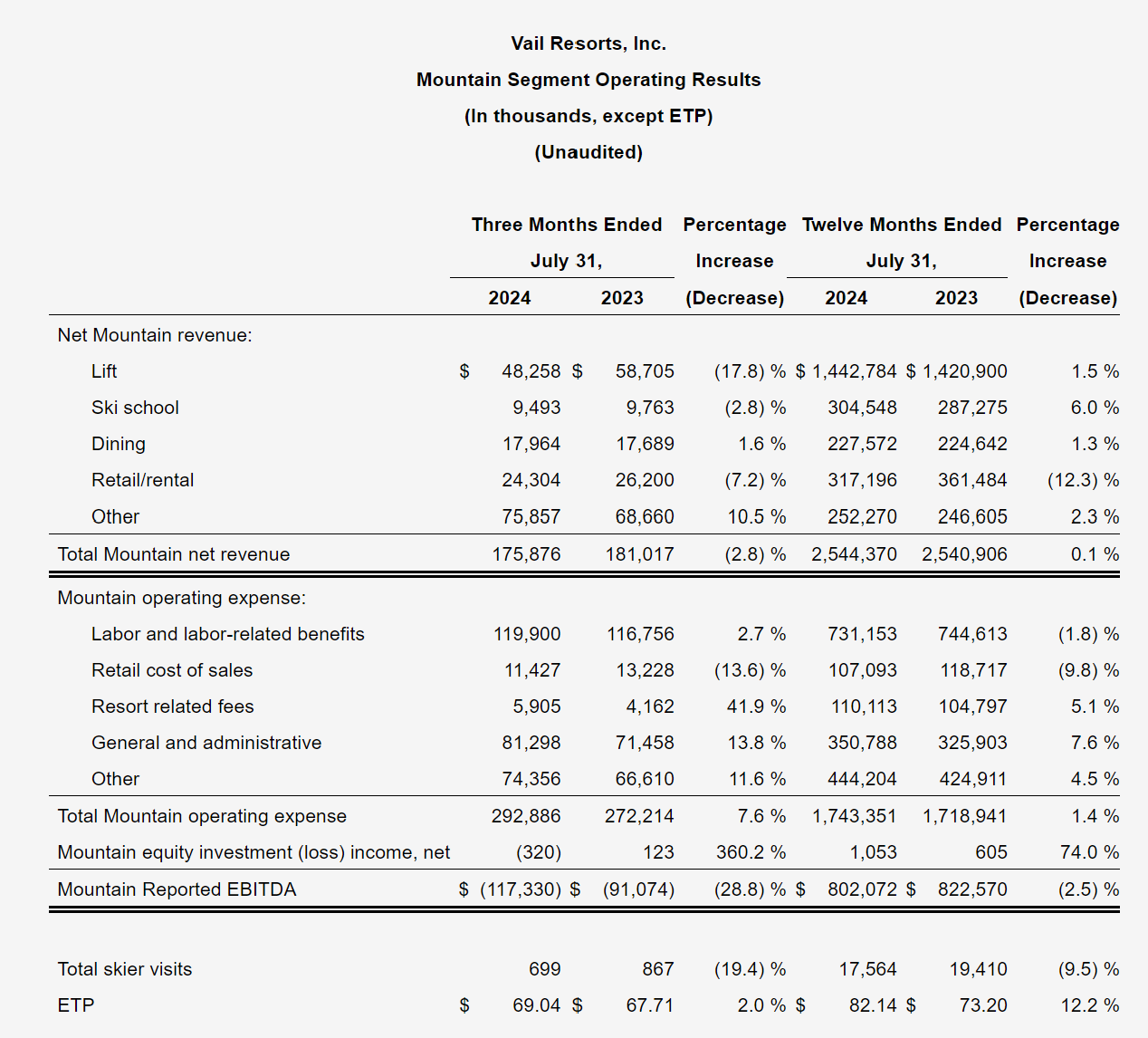

How does Vail make its money? Well, if you’ve been paying attention to costs of skiing over the past few years, you’d probably think that lift tickets are a big component, and you’d be right. For the Fiscal Year from August 2023-July 2024 (FY ‘24), Vail Resorts recorded $1.44 billion in Lift ticket revenue, which is up 1.5% from the ‘23 Fiscal Year. This includes the incredibly popular Epic Pass products.

One notable decrease in revenue is in the Retail and Rentals field, which totaled $312 million for FY ‘24. This is a huge 12.3% drop from FY ‘23, totaling around $44 million less in revenue. It’s hard to say for certain what caused this, but the drop in skier visits is likely the main culprit, as less people on the slopes also means less people in the stores looking for new skis or renting for the day.

Other large contributors to revenue include Lodging at $336 million (down 1.3% from ‘23), Ski School at $305 million (up 6%), and Dining at $228 million (up 1.3%). This all adds up to a Net Revenue of $2.89 billion, which is surprisingly down just 0.1% from FY’23.

Why is it remarkable that the revenue is down that little? Well, skier visits were down 9.5%, from 19.4 million to 17.6 million. It’s no secret that last winter was not the best snow wise, and the drop among Vail-owned resorts was greater than the US nationwide skier visit drop from ‘23-’24, which was 7.6%.

One major reason for this drop was the horrible season for Midwest hills, especially in the Lower Midwest. In this region, the natural weather was an absolute disaster. Hills such as Mad River Mountain and Alpine Valley in Ohio, Snow Creek and Hidden Valley in Missouri, and Paoli Peaks in Indiana all had some of their shortest seasons on record. This very well may have impacted other regions as well, as local skiers to those hills may have canceled trips out west after seeing the dissuasive conditions at hand. Compared to other multi-mountain companies such as Alterra, Powder, or Boyne, Vail found itself with considerably more exposure in the Midwest last season. Vail Resorts owns far more Midwest mountains than its competitors—with nine under its belt—compared to the other companies owning a combined three. According to the NSAA, the Midwest as a whole saw a 26.7% drop in skier visits from last year, which was the most of any US region, and you can learn more about the Midwest’s rough winter here.

But despite this huge drop in skier visits, one number that helps explain why the revenue barely dropped is the ETP, or Effective Ticket Price. This is the average amount a skier pays for one day of lift access across all Vail Resorts-owned mountains, and the metric is found by dividing Lift revenue by skier visits. It’s important to note that ETP takes into account all forms of access, ranging from insanely expensive day ticket purchases to Epic Pass holders skiing over 100 days and getting the bargain of a lifetime.

You probably already know where this is going—while skier visits were down, Vail’s ETP most certainly was not. The ETP for FY ‘24 was $82.14, which is a whopping 12.2% increase from the FY ‘23 tally of $73.20. A big reason for this was the steep increase in regular lift ticket prices; while Epic Season and Day Pass prices only increased by around 8% versus the prior year, regular lift ticket prices increased a lot more. Although the average lift ticket prices at already-expensive places like Vail and Beaver Creek went up by less than 10%, destinations that used to be slightly more reasonable saw massive price changes. For example, the weighted average lift ticket prices for each of Northstar, Heavenly, Stowe, Stevens Pass, Park City, Keystone, and Okemo went up by over 15%, while the weighted average ticket price for Whistler Blackcomb, which is the company’s only Canadian resort, went up by a staggering 36% from $144 USD to $196 USD.

It seems that the trend of declining visitation but increased revenue may continue next season, albeit potentially to a lesser extent. A couple weeks ago, it came out that Vail Resorts’ 2024-25 Epic Pass sales through the summer dropped 3% compared to the prior year, although pass revenue was actually up 3% thanks in part to another 8% across-the-board price increase for the passes this season. It actually seems that this summer’s sales saw some improvement from the early-bird spring renewal period, with existing passholders making up their minds later than usual, but fewer new passholders than in years’ past. Especially when considering that the company’s mountain portfolio hasn’t changed all that much in the past five years, it’s possible that Vail has hit its ceiling for growth in the North American market. For now, Vail Resorts may be able to keep its revenue flat by continuing the price increases, but this strategy does not seem like a winning one for the long term.

It’s also worth briefly touching on Vail Resorts’ lodging revenue from last year. While this segment did drop slightly from the prior year overall, the changes by lodging type have been more drastic. The hotel, transportation, and golf sections of Vail’s portfolio saw growth of 4.8%, 7%, and 7.7% respectively, while the Vail managed condos saw a decrease of almost 11% from FY ‘23. The decrease in condo revenue tracks with the lower visitation, but it’s somewhat surprising to see revenue from hotel rooms continue to grow despite last year’s trends. But upon a closer look, it becomes apparent why: the increase in hotel revenue came in large part thanks to increased visitation at Grand Teton Lodge Company, which provides accommodations that only operate during the summer months. So yeah, Vail Resorts’ winter lodging took a huge hit as expected, but the company was actually able to hedge on this with a sizable boost in summer visitation—albeit to accommodations that most people don’t even know they own.

But perhaps the most shocking thing in Vail’s earnings report is what we see with ski school and dining. Despite the double-digit drop in retail and rentals, the ski school and dining both actually went up in revenue for FY ’24 vs. FY ‘23. Dining went up by a modest 1.3%, but ski school revenue actually increased by a pretty eye-opening 6%. And unlike with lodging, there wasn’t a summer offset to boost these metrics; Vail Resorts claims that these revenue increases were due to an increase in guest spending per visit at their resorts. But then when you look at the fact that dining and lessons are still recovering from the COVID era—and that 1-day lessons could cost as much as $1,560 at Vail’s highest-end resorts last winter—maybe this makes a little more sense.

Finally, given the massive drop in rental revenue, it’s also worth briefly touching on Vail Resorts' highly-publicized introduction of My Epic Gear, a membership program intended to offer access to premium ski and snowboard rental equipment on a subscription-level basis. In its inaugural year, My Epic Gear was anticipated to enhance guest experiences and drive revenue. However, the short-term contributions for the program, which was piloted at a handful of destinations last year, seem to have been modest, leaving it unclear whether it helped offset the significant drop in revenue in the rentals category.

FY ‘24 Expenses

What’s costing Vail Resorts the most? Well, like most companies, its employees. On the mountain side of things, labor costs made up around 42% of operating expenses, or $731 million out of $1.74 billion. Next is the “Other” category, which can include typical maintenance at a ski area, such as fixing up snowcats to putting new paint up on the lodge. The “Other” category makes up $444 million, which is up from the $424 million expense in FY ‘23.

In lodging, there was a bit more movement, with lodging expenses dropping by 4.6% from $328 million to $313 million. This was largely due to drops of over 6% in both Payroll and General and Administrative expenses versus the previous fiscal year, which, in other words, was basically the company employing fewer hotel and condo workers to account for the decrease in demand. As we’ll discuss later in this article, this decrease in employment may be an omen of things to come.

FY ‘24 Net Income

If you take Net Revenue and subtract Net Expenses, what do you get? EBITDA of course! EBITDA, or “earnings before interest, taxes, depreciation, and amortization”, may not be the most simple statistic on the surface, but it allows us to get to one of the best measures of something that’s a lot easier to understand: Vail Resorts’ profitability.

In FY ‘24, Vail’s EBITDA was $827 million, a small drop from FY ‘23 when it was $833 million. However, the way the company got to this number this past fiscal year changed a bit versus the year before. Mountain operations EBITDA decreased by $20 million from ‘23 to ‘24, but Lodging EBITDA increased by over $10 million, which was thanks in large part to both the summer revenue and the decrease in in labor costs we mentioned earlier. The decrease in Mountain operations is largely due to the $44 million drop in Retail and Rentals revenue, as we also detailed above.

Ultimately, Vail Resorts made over $230 million in Net Income during FY ‘24, which is slightly down from FY ‘23, when the Net Income was $268 million. Still, $230 million isn’t chump change, and when you compare that to where Vail Resorts was a few years ago, the change is substantial.

Trends since COVID

While the trends from FY ‘23 are interesting on their own, they only show a snapshot of the whole story. Vail Resorts has seen massive changes over the past five years, with more than 20% growth in ETP, over 30% growth in total skier visits, over 40% growth in total revenue, and over 130% growth in Net Income attributable to Vail Resorts since FY ‘20. Now, FY ’20 was greatly affected by the COVID pandemic—and a handful of small Northeast resorts and European regions have been added to the Vail Resorts portfolio within the past four years—but even year-over-year growth has been largely consistent since then, with the only slowdown coming in the past year.

Stock Price Decrease

So if Vail Resorts has maintained pretty consistent revenue over the past year, why has its stock price gone down so much? As a public company, Vail sells stock on the New York Stock Exchange under the ticker symbol MTN. This stock reached its peak in 2021, selling for over $370 per share, but has dropped substantially since then, and is now at under $178 per share. This is despite the huge growth numbers seen during 2022 and 2023.

Well, steady growth and staying flat may seem good on the surface, but a large part of a company’s stock price involves speculation; in other words, what really matters is how Vail Resorts is positioned for the future. Stockholders had been banking on a continuation of previous growth, and Vail’s profit forecasts came in lower than expected due to the factors we mentioned earlier. Snow conditions have been less reliable in recent years, with the Midwest and Australia facing the biggest challenges this past fiscal year, and investors are noticing.

“Resource Efficiency Transformational Plan”

So while its income may not have changed all that much versus the year before, Vail Resorts is a public company, and whether you like it or not, that ultimately means that company’s fiduciary duty is to its shareholders. The company had to figure out some way to pump up its stock, and the same day as the release of the FY ‘24 Fiscal Review, Vail Resorts released a “Resource Efficiency Transformational Plan”, and they kind of buried the lede in their fiscal review. In a separate press release, they state the Transformational Plan will focus on cost efficiencies, which will include “Position eliminations, impacting less than 2 percent of the company's total workforce, including 14 percent of its corporate workforce and less than 1 percent of the company's operations workforce.” So if you’re currently working at Vail in Broomfield CO, you may want to start looking for a new job.

Vail Resorts CEO Kristen Lynch went on to say, “No matter how big or small the impact of position eliminations, we do not take lightly any decision that affects our team members.”

Executive Compensation

Being a public company, Vail also releases the compensation for the executive board. So, let’s see how much CEO Kristen Lynch is paid, and how that compares to the average employee.

During FY ‘22, FY ‘23, and FY ‘24, Kristen Lynch earned more than $6 million in compensation, in a large part owing to Stock Awards and Option/Share Appreciation Right Awards. Compared to the former CEO of Vail Resorts, Robert Katz, Mrs. Lynch is making almost 60% more than any of his last three years as CEO (in 2021 he made $3.8 million).

But all CEOs make an absurd amount of money, right? So how does the CEO’s compensation compare to the median employee? Vail also releases the ratio of pay between the CEO and median employee. In FY ‘21, that ratio was 94:1, and it dropped to 79:1 during the 2022 Fiscal Year. However, in FY ‘23 that ratio skyrocketed to 128:1 before dropping back to 112:1 in FY ‘24.

While Kirsten Lynch’s salary has remained relatively stable over the past three years, the median employee salary has been all over the place. For the ratio of pay formula, Vail Resorts normalizes median pay to a full year, as many employees are seasonal due to the nature of ski resort jobs. In FY ‘22, the median annual salary for a Vail Resorts employee was $70,375, which dropped to $48,511 in FY ‘23, the bounced back to $56,109 in FY ‘24. It’s especially interesting to see this discrepancy swing in the downward direction in recent years given that the company raised their minimum wage across all positions to $20/hour for FY ‘23.

Now, compared to the average pay ratio for companies on the S&P 500 is 268:1 (AFL-CIO), so Vail is far from the worst offender, but it’s not a good look for your CEO to be making more than ever during the past few years, having a year with near-flat growth, and firing 14% of your corporate workforce.

How Vail Resorts’ Financials Will Impact Its Ski Resorts

So Vail Resorts’ revenue growth basically petered out this year, so what does that mean for the future of its resorts? Well, the company’s on-mountain capital investments have significantly declined over the past two years. In 2021, when the stock was at its peak, Vail announced nearly 20 new lifts set for completion in the following year. Now, they’re adding fewer than five lifts annually.

Unlike the game-changing investments seen at Keystone, Beaver Creek, and numerous other resorts in past years, only two locations—Hunter and Whistler Blackcomb—are getting new lifts this year. Next summer, the only planned lift installation across the entire Vail Resorts portfolio is the new Sunrise Gondola on the Canyons side of Park City. While the high investment levels of the early 2020s may not have been sustainable, this sharp decline has certainly raised eyebrows.

This decline becomes especially apparent when you look at the number of lifts Vail Resorts operates across the world—over 200—and, furthermore, the number of lifts reaching the end of their useful lives—which, if you generously only look at high-speed detachables that are over thirty years old, still totals over two dozen. Vail Resorts is going to need to replace these lifts at some point in time or another to meet basic lifecycle requirements, and if the rate of replacement over the next two years becomes the norm, the medium-term future for the company is not going to be pretty.

One place that may see renewed investment, however, is Vail Mountain itself. The long-anticipated West Lionshead base area now appears to be finally happening. Not only will this base area provide a new way for visitors to access Vail’s 5,300 acres of skiing, but more importantly, it will provide more workforce housing, which is incredibly hard to come by in the notoriously expensive and arguably-NIMBY-controlled town of Vail.

Final Thoughts

So on the surface, FY ‘24 was far from the worst year it could have been financially for Vail Resorts. The company weathered the lower snowfall across multiple regions with record ticket revenue and remained profitable, achieving more than $230 million in net income. But serious concerns have surfaced about the long-term sustainability of the company.

For the average person visiting a Vail Resort this next season, the company’s spending decisions may be a bit head scratching. Those skiing down Riva Ridge or dropping into the A-51 terrain park won’t notice a difference in Kristen Lynch’s stock options, but they may notice some lifts getting a little older, and maybe some operational hiccups with the loss of 14% of the corporate office. But ultimately, CEO pay at large public companies is often designed to keep top-level executives motivated during stressful times, and Vail Resorts is no exception. The company might be okay with putting off some investments or removing lower-level corporate positions, but the stability of the CEO job, whether you like it or not, is a top priority for a publicly-traded firm like this. Whether these decisions blow up in their face over the next few years, however, is still yet to be seen.

What should we expect for the ski industry as a whole?

The next few years will be incredibly important not only for Vail Resorts, but the ski industry at large. Love it or hate it, Vail Resorts has a huge impact on the ski industry, and if they are on the decline, many others in the industry will likely suffer as well. Also, while the other ski resort mega corporations do not have publicly available financials, Vail is far from the only company pulling back on investments—the company’s main competitor, Alterra, has scaled back quite a bit on new lifts over the next year or so, and an additional competitor, Powdr, is selling off several ski resorts in its portfolio, which is totally unprecedented within today’s ever-consolidating ski world. While investors are bearish on Vail, we’ll see if the company can turn itself around with more large investments, earning back the trust of skiers and investors alike, and maintaining its status as the top mountain operator in the world.